A Junior Silver Explorer Beside a Sleeping Giant

Drill results could change everything.

Not investment advice. Disseminated on behalf of Americore Resources (TSXV: AMCO).

There aren’t many true ground-floor silver stories left in North America. Not the recycled assets. Not the “maybe someday” conceptual targets.

I’m talking about a real project with real past production, sitting in Nevada, tied to one of the largest mining companies on the planet.

That’s Americore Resources (TSXV: AMCO), a C$5.7 million micro-cap that just transformed itself through a strategic reboot and an unexpected partnership most juniors could only dream of.

And the setup here is almost unfair.

Silver is in a full-blown supply squeeze. Producers are struggling to replace reserves. The energy transition is accelerating demand faster than anyone projected. Prices ripped toward US$50/oz this year. Yet Americore is quietly sitting at 37 cents, controlling a project that once produced 5 million ounces and still carries a historic 28-million-ounce silver resource.

This is exactly the type of asymmetry retail investors look for when the metal cycle starts heating up.

The story starts with Newmont

Last fall, when Americore was still operating as K9 Gold, the company secured an exploration and purchase option with Newmont Corporation.

Yes, that Newmont—the world’s largest gold miner.

This wasn’t a photo-op partnership. Newmont didn’t just hand over some land and walk away.

They kept equity. They retained a royalty. They put their name on the deal.

That alone is a massive credibility boost for a company this size.

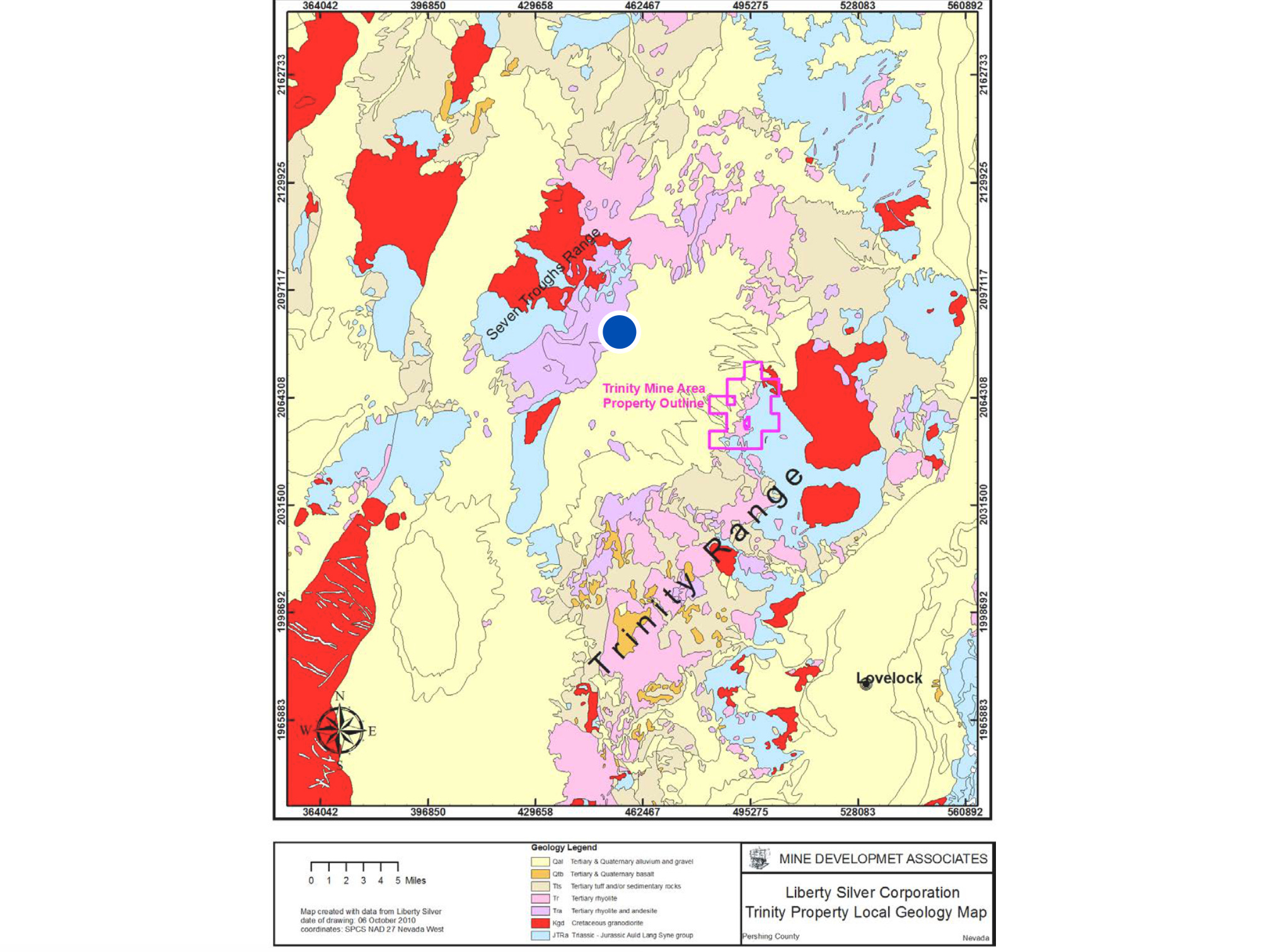

The project they handed off is Trinity Silver, a past-producing mine with infrastructure, data, and a history of high-grade silver that was never fully followed up with modern exploration. The upfront acquisition cost?

Only US$50k and 100k shares.

That is unheard-of for a Nevada silver system with real past production.

It’s a classic case of a major moving on, and a small, hungry explorer stepping in to finish the job.

Why Trinity matters

Silver producers are running into a wall. They are consuming reserves faster than they can replace them. Meanwhile, demand from solar, electronics, and electrification has gone parabolic.

The result: one of the tightest silver markets in decades.

Americore’s Trinity Project already has what most juniors spend years trying to prove.

A historic 28-million-ounce silver resource.

A past-producing open pit.

Lead-zinc credits that could materially improve economics.

And a district-scale trend that still has open extensions.

Americore isn’t drilling blind. They’re drilling where silver has already been found.

The strategic reset that changed everything

Before the Newmont deal, the company was scattered across multiple projects.

Then, management did something very few juniors are disciplined enough to do.

They hit the reset button.

Non-core projects were optioned off.

A planned financing was cut in half to protect the structure.

The name was changed to Americore Resources to reflect a singular focus on silver.

The share count was kept exceptionally tight—around 19 million shares outstanding.

This leaves Americore with a clean path forward, no debt, and a micro-float structure that amplifies any major news.

Drill results will be the make-or-break moment

This is a binary story, and management isn’t pretending otherwise.

The upcoming drill program will target extensions around the historic Trinity pit and test areas that previous operators never fully explored.

If Americore hits high-grade silver near surface, the re-rating could be dramatic.

Trinity doesn’t need to be perfect. It only needs to be good enough to move a C$5.7 million company into the next tier.

How the market could revalue Americore

Let’s do a simple comparison.

Peers with similar silver exploration stories trade at:

Summa Silver ~C$50M

Reyna Silver ~C$36M (recent acquisition)

Americore ~C$6M

Even assigning a conservative valuation of C$0.67 per ounce of in-situ silver puts Trinity around C$18–20 million.

That’s 3–4x today’s valuation before new drilling adds anything.

Our 12-month target sits at C$1.00, based on partial validation of the historic resource and the market recognizing the discovery potential tied to Newmont’s involvement.

What could go wrong

As with any junior explorer, drill results are the ultimate judge.

Americore will need additional capital as it advances the project.

And with a single asset, there’s no plan B.

But that’s the nature of asymmetric plays: the risk is clear, and the reward is tied directly to the drill bit.

The bottom line

Americore is a microcap with a major’s fingerprint on its flagship asset.

It controls a past-producing silver project in Nevada, one of the safest mining jurisdictions in the world.

It has a tight structure, a clean strategy, and an upcoming drill program that could redefine the company.

In a silver bull market where new discoveries are scarce, Americore offers early-stage exposure with real validation behind it.

It’s speculative. It’s early. But it’s the kind of story that can move fast when the pieces come together.

Disclaimer:

“This newsletter was conducted on behalf of Americore Resources Corp, and was funded by CAPITALIZ ON IT. Cashu Technologies has been compensated five thousand dollars for this newsletter. I only express my opinion based on my experience. Your experience may be different. This newsletter is for educational and inspirational purposes only. Investing of any kind involves risk. While it is possible to minimize risk, your investments are solely your responsibility. It is imperative that you conduct your own research. There is no guarantee of gains or losses on investments. Please do your own due diligence. I am not a financial advisor, and this is not a financial advice channel. All information is provided strictly for educational purposes. It does not take into account anybody’s specific circumstances or situation. If you are making investment or other financial management decisions and require advice, please consult a suitably qualified licensed professional.

The securities of Americore Resources Corp are speculative, and the company has not yet achieved consistent positive cash flow from operations. As a growth-stage company, it anticipates negative cash flow for the foreseeable future as it focuses on development and commercialization efforts. Parties viewing this video should thoroughly review the company’s public disclosure and documents available on sedarplus.ca.

See full disclaimer here: https://capitalizonit.com/amco