Gold Is Breaking Records. But Not All Gold Stocks Are the Same.

Gold isn’t creeping higher. It’s ripping.

Not investment advice. Disseminated on behalf of Revival Gold.

Gold is moving like it has something to prove

For most of the last decade, gold felt like a “someday” asset. It moved when markets got scared, then drifted back into the background while investors chased growth, AI, crypto, anything that felt more alive.

That’s not what’s happening now.

After a huge 2025 run, gold has been trading at or near record highs, recently around the mid-$5,000s per ounce. When a metal moves like that, it stops being a headline and starts becoming a force. It changes how money behaves. It changes what projects make sense. And it changes which companies the market is willing to take seriously.

This is the moment when the market starts looking past “what could be found” and back toward “what already exists.”

Because in gold cycles, the biggest shifts often don’t happen in exploration first. They happen in leverage… Companies with real ounces in the ground, real studies on the shelf, and real paths toward production that suddenly look a lot more attractive when the gold price is high.

That’s the lane Revival Gold sits in.

Revival isn’t trying to discover gold. It’s trying to restart it.

Revival Gold (TSX-V: RVG | OTCQX: RVLGF) is a U.S.-focused gold developer built around something most retail investors intuitively understand: the world is full of assets that were left behind not because they failed, but because the timing was wrong.

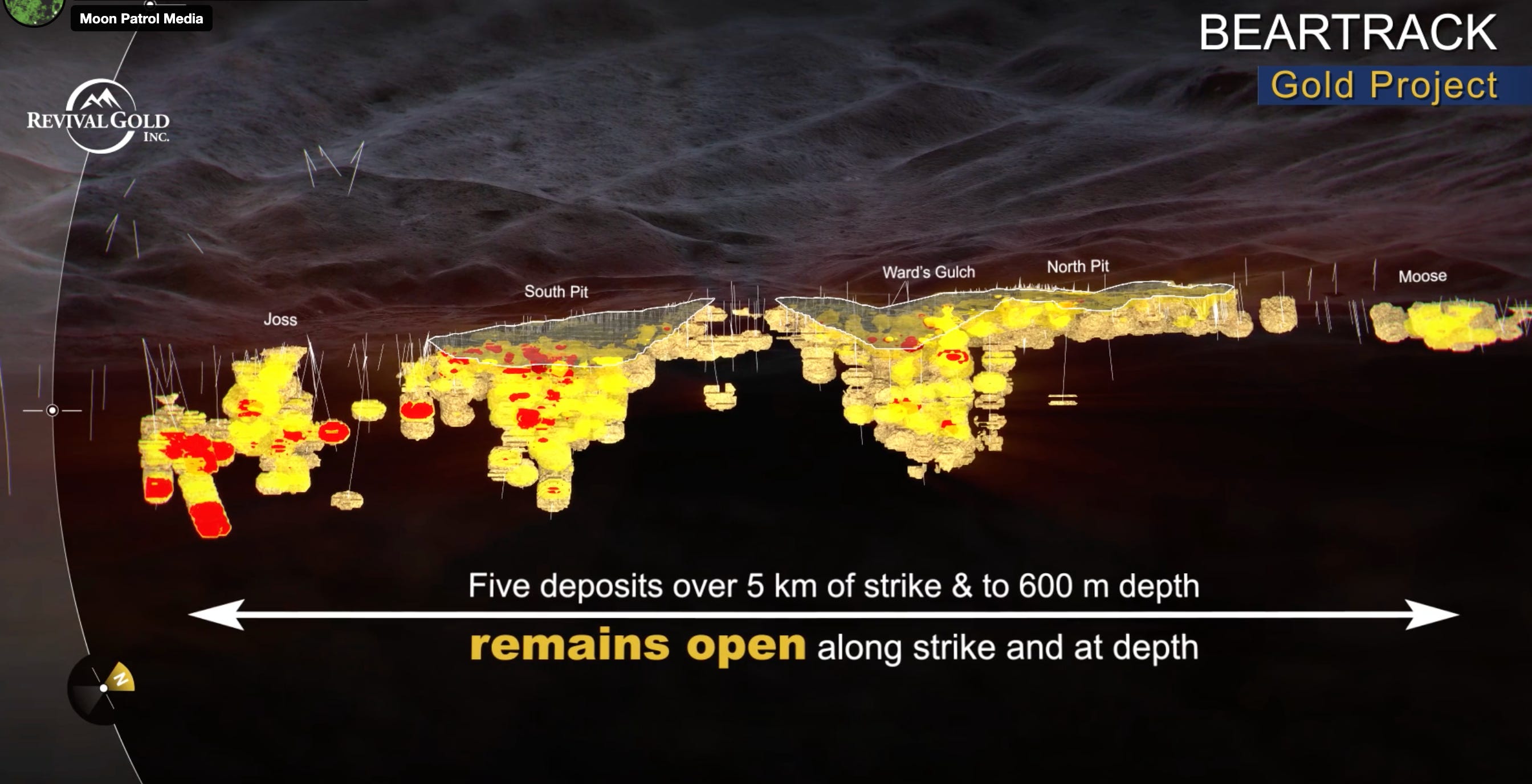

Revival controls two past-producing gold projects in the western United States. Mercur in Utah and Beartrack-Arnett in Idaho, and together they host roughly 6 million ounces of gold in resources, according to NI 43-101 technical reports (measured, indicated, and inferred categories).

These weren’t theoretical systems. They produced. They had operating histories. They mattered when gold was dramatically lower than it is today.

And then the cycle turned.

Projects like these don’t always die because the ore disappears. Sometimes they go quiet because the math breaks. Costs rise. Prices fall. Capital leaves. The industry moves on.

But the gold stays.

Why this moment feels like an inflection point

Here’s the part most investors miss until it’s already obvious: when gold is high, the companies that begin to move aren’t always the ones with the most exciting drill story. It’s often the ones that can point to real ounces and say, “Here is what this could be worth under a higher gold price scenario, based on public studies.”

That’s why developers can become the market’s focus during certain windows. They aren’t selling a dream. They’re advancing a plan.

Revival has done the work to put real numbers on the table. In the company’s published economic studies, Mercur’s after-tax NPV (5%) is estimated at ~US$741M at $3,000 gold, and rises above US$1.2B at $4,000 gold (per the 2025 PEA). Company materials also show that at $4,000 gold, the combined after-tax NPV (5%) of Mercur + Beartrack-Arnett is approximately US$2.1B.

That’s not a promise of value. It’s model output, based on assumptions that can change. But the point is simple and powerful: when gold prices move higher, projects that once looked “okay” can start to look meaningfully different on paper. And the market often re-prices that possibility before anything is built.

Revival’s market cap has recently been around the US$160M range in its January 2026 investor materials. That kind of contrast between a small-cap valuation and large modeled project value is exactly why “leverage” names tend to show up on more watchlists when gold is strong.

Two projects, two different strengths

Mercur, Utah is a past-producing open-pit mine that historically produced about 2.6 million ounces of gold. One detail that matters (even for non-mining investors) is that it sits largely on private patented land, which can simplify certain aspects of the path forward compared to projects dominated by federal land.

The 2025 PEA outlines a potential modern heap-leach operation targeting approximately 95,000 ounces per year for 10 years, with economics that improve at higher gold price assumptions. The company’s roadmap includes more drilling and metallurgical work, moving toward a Pre-Feasibility Study and permitting.

Beartrack-Arnett, Idaho is another past producer with existing roads, power, and site infrastructure. A 2023 PFS outlines a restart heap-leach plan targeting roughly 65,000 ounces per year over 8 years, and the project also carries underground expansion potential, particularly in the higher-grade Joss zone that the company continues to drill and evaluate.

Even if you’ve never invested in mining before, this distinction is easy to understand: these aren’t “maybe someday” grassroots claims. These are projects with history, studies, and a clear direction of travel.

The quiet part that matters: funding and credibility

Revival reports roughly C$18M in cash in its latest deck, which management indicates is being used for drilling, metallurgical work, and other de-risking efforts—without an immediate need to finance.

And the shareholder base includes groups like Dundee Corporation and EMR Capital, names that are known in the resource development world.

That doesn’t eliminate risk. But it does help answer an important retail question: “Is this a real plan, with real support, or just a story?”

The core of the setup

If you strip away the technical language, Revival’s story is pretty human.

It’s about two American gold projects that already had their moment once, then got put on pause when the world changed. And now, in a gold market that’s rewriting what’s economically possible, the story is restarting with modern studies, modern work programs, and a clearer path than most early-stage explorers can offer.

Development is execution-driven. Permitting matters. Costs matter. The gold price matters.

But urgency doesn’t come from certainty.

It comes from timing.

And right now, the timing is forcing investors to ask a simple question:

When gold is this high, which companies already have the ounces, the studies, and the jurisdiction to matter?

Revival Gold is one worth understanding while the story is still being written—not after the crowd arrives.

Disclaimer: Disseminated on behalf of Revival Gold. Cashu Technologies was compensated by Resource Stock Digest on behalf of the company for the creation and distribution of this newsletter. This newsletter is for informational purposes only and is not investment advice. The content is based on public company materials, including NI 43-101 technical reports and investor presentations. Economic studies such as PEA and PFS are preliminary in nature and include assumptions that may not be realized. Always conduct your own due diligence and consult a licensed financial professional before making investment decisions.