Is This Oilpatch Underdog Ready to Gush?

Drill, Drill, Drill

Prairie Operating Co. (NASDAQ: PROP) may not be a household name yet, but this up-and-coming oil & gas producer is making bold moves that have bullish investors taking notice. From surging production guidance to a transformative acquisition, Prairie is positioning itself as a nimble player riding the energy sector’s tailwinds.

Let’s dive into why this small-cap driller could strike it big in the broader oil boom – and why recent developments have us optimistic about its growth potential.

This is a sponsored report, see disclaimer below.

Recent Developments Fueling Prairie’s Ascent

Prairie is making big moves—and Wall Street is paying attention. This once-small oil player has unleashed a massive growth story, issuing sky-high guidance, sealing a game-changing acquisition, and locking in the funding to fuel its expansion. The result? A stock that’s soaring and a company that’s quickly becoming a serious force in the energy sector.

👆 Big Guidance, Big Gains: Prairie kicked off 2025 with a bang, projecting 7,000–8,000 BOEPD—a near 300% production surge. That kind of growth fuels a massive turnaround, with net income expected to hit $69M–$102M. Investors took notice—shares spiked nearly 50% on the news.

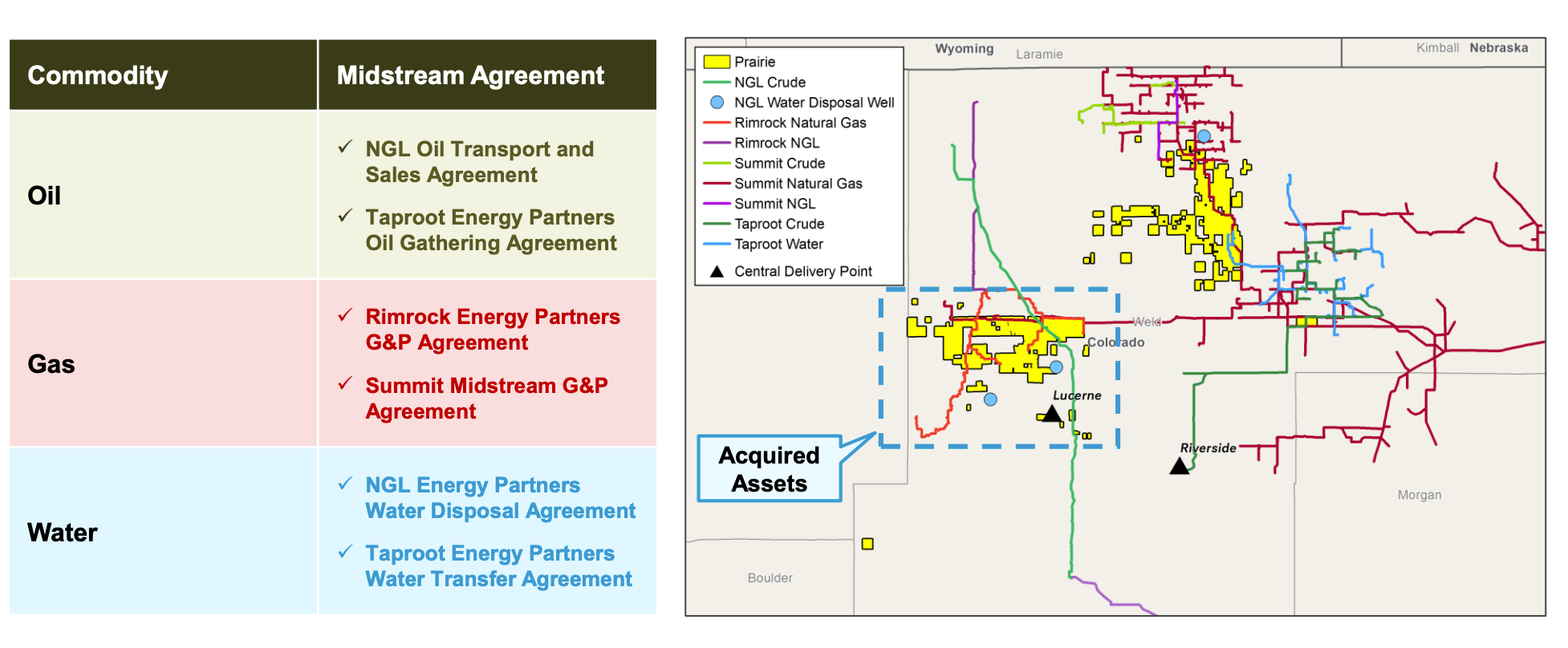

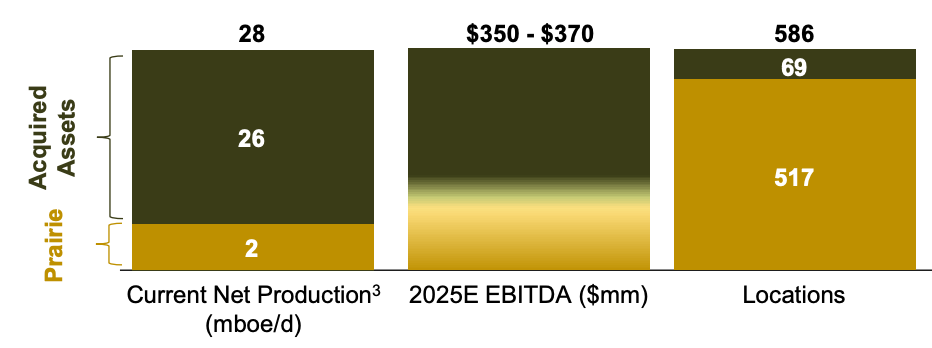

⛏ DJ Basin Game-Changer: Prairie isn’t just growing—it’s supercharging its portfolio. The company is buying prime DJ Basin assets from Bayswater for $602.75M, adding 26,000 BOEPD—mostly high-value liquids. Once the deal closes, Prairie’s output quadruples to 29,000–31,000 BOEPD. The deal also delivers $1.1B in reserves, instantly turning Prairie into a serious mid-tier producer.

🚀 Fully Funded for Takeoff: To power this expansion, Prairie secured $1B in financing, including a $44M initial commitment from Citi. It also raised $200M through a stock offering. While dilution concerns led to a temporary 24% drop in shares, the fresh capital ensures the deal gets done—and sets Prairie up for more growth.

Bottom line? Prairie isn’t just growing—it’s exploding onto the mid-cap scene. Let’s dive into how it stacks up against industry heavyweights.

Prairie’s Winning Formula: The Right Assets, The Right Strategy

Prairie is playing a smart, strategic game in one of the most attractive U.S. oil basins. By locking in premium acreage, focusing on high-margin production, and securing top-tier financial backing, Prairie has positioned itself for breakout success. Let’s take a look at some of it’s key assets:

➡️ Building Scale in the DJ Basin

Prairie is laser-focused on Colorado’s DJ Basin, a region with proven reserves, strong infrastructure, and oil-friendly policies. The recent $7.6B Chevron-PDC deal confirmed its value, and Prairie’s 54,000 net acres give it serious scale. Sticking to a single core region means lower costs, better efficiency, and a competitive edge in local drilling expertise.

Read more about the DJ Basin Assets here.

➡️ Oil-Weighted Production = Higher Margins

Not all barrels are created equal, and Prairie has a key advantage in the type of hydrocarbons it produces. The company’s existing output and the newly acquired assets are heavily oil-weighted (approximately 69% liquids), which generally command higher prices and margins than natural gas. In an environment of solid oil prices, Prairie’s oil-centric production mix means stronger revenue per BOE relative to gas-heavy peers. This tilt toward liquids gives Prairie a profitability edge and more cash flow to reinvest in growth or return to shareholders down the line.

➡️ A Lean and Focused Growth Strategy

Unlike bloated majors, Prairie operates lean and fast. Its strategy? Pick up high-quality assets from private sellers, develop them, and unlock value. This roll-up model lets Prairie scale quickly while competitors stay cautious. With a management team stacked with industry veterans, the company is betting that aggressive growth in a top-tier basin will pay off big.

➡️ Financial Firepower To Support Expansion

Prairie isn’t just making moves—it has the cash to back them up. A $1B credit facility from Citi ensures liquidity for development, while a stock-based Bayswater deal signals insider confidence in future upside. Unlike many cash-strapped micro-caps, Prairie has the balance sheet to fund expansion at full speed.

Growth Catalysts Powering Prairie’s Upside

Prairie’s bullish thesis doesn’t rest on hope alone – there are concrete catalysts and tailwinds that could propel the company in the coming years. Here are several factors stacking the odds in Prairie’s favor:

1️⃣ Surging Production & Earnings

Prairie’s forecast production is set to explode higher, driving a swing to strong profitability. The company projects reaching 7,000–8,000 BOEPD in 2025 (up ~300% YoY), which in turn underpins expected net income of $69–$102 million. Rapid volume growth means Prairie can quickly scale into its cost base, boosting margins. Hitting these targets would make Prairie one of the faster-growing oil companies around, a status that typically attracts investor interest (and higher valuations).

2️⃣ Transformative Acquisition Boost

The Bayswater asset purchase is a game-changer that will supercharge Prairie’s metrics once closed. It brings ~26,000 BOE/day of current production and nearly 78 MMBOE in reserves (PV-10 ~$1.1B) onto Prairie’s books. Instantly, Prairie’s output and reserves will be several times larger, supporting much higher revenue and cash flow in 2025 and beyond. Crucially, the acquired wells and future drilling locations are highly oil-rich (69% liquids), meaning Prairie is acquiring quality barrels that should generate strong cash margins. This deal is highly accretive by almost any metric – from cash flow to reserves per share – setting the stage for significant earnings growth once Prairie integrates the new assets.

3️⃣ Massive Drilling Inventory

With the combined acreage from Nickel Road and Bayswater, Prairie now controls a multi-year inventory of drilling locations on ~54,000 net acres in the DJ Basin. In the Nickel Road deal alone, Prairie gained 89 fully permitted well locations ready for development. The Bayswater acreage adds dozens more future well sites across proven geologic sweet spots. This ample inventory gives Prairie the optionality to sustain output growth year after year. Management can high-grade its drilling schedule, tapping the most promising locations first and continuously renewing its production pipeline.

4️⃣ Favorable Oil Market Tailwinds

Oil prices remain strong (~$80/barrel in early 2025), backed by resilient demand and OPEC’s tight supply management. Even if prices dip, forecasts still peg U.S. crude in the ~$70 range—well above Prairie’s breakeven. That means its oil-heavy production keeps spinning off cash for growth or debt reduction.

Meanwhile, global oil demand remains steady, ensuring Prairie’s new barrels will have willing buyers. The industry’s wave of M&A—Chevron, Exxon, and others snapping up independents—highlights the value of proven reserves. With its growing DJ Basin footprint, Prairie could one day attract buyout interest itself. For now, strong oil economics provide a solid foundation to execute its game plan.

5️⃣ Robust Financial and Operational Support

Prairie isn’t just relying on oil prices—it’s built a solid foundation. A $1B credit facility from Citi provides financial flexibility for development and stability through commodity swings. It’s also gaining experienced teams from Bayswater and Nickel Road, easing integration and ramp-up. Plus, a strong focus on safety and community relations helps keep regulators and locals onside, avoiding hurdles that trip up other drillers. These “soft” factors—capital, expertise, and reputation—are key enablers for unlocking the full value of its assets.

Each of these catalysts contributes to a bullish outlook. If Prairie delivers on even a few of these fronts, the upside could be substantial. And notably, the company is already checking multiple boxes: production is set to jump, a big acquisition is underway, and oil prices remain supportive.

The Undiscovered Underdog?

Prairie is still off most investors' radar, but that may not last long. With insiders buying in, undervalued shares, and a limited but bullish analyst outlook, this stock looks like a classic underdog story in the making.

Share Price Swings = Opportunity

After surging 50% on January’s guidance update, dilution fears knocked the stock down 24%. It’s since rebounded, but at ~$7–$8, it’s still well below its 52-week high of ~$16. For investors who believe in Prairie’s trajectory, this could be a rare chance to buy before the story fully unfolds.

Insiders Are Betting Big

Director Jonathan Gray just scooped up over $1.2M in stock at ~$6 per share—serious conviction from an experienced energy investor. When those with inside knowledge put their own money on the table, it’s usually for a reason. This isn't just a vote of confidence; it’s a signal that those closest to the business see it as deeply undervalued.

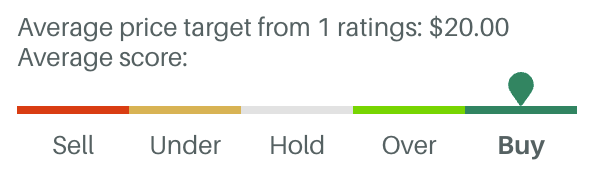

Wall Street Coverage is Sparse – For Now

Only one analyst covers Prairie, but they’ve slapped a $16 price target on it—more than 110% upside. Small coverage means the stock is still undiscovered, but as Prairie executes and institutions take notice, fresh buy ratings could fuel a rerating.

Right now, Prairie fits the profile of an under-the-radar growth play: a volatile stock, overlooked by analysts, with insiders quietly buying in. If it delivers, the market won’t ignore it for long.

The Bottom Line

Prairie Operating Co. has rapidly evolved from an obscure startup into a serious contender in the oil patch. The company’s strategic bets – doubling down on the DJ Basin, acquiring quality assets, and ramping production – are falling into place, and early results look promising. In the context of a strong energy sector, Prairie offers a rare growth story: while many oil companies are content with slow-and-steady outputs and rich dividends, Prairie is growing volumes at triple-digit rates and increasing its reserves base dramatically. That kind of expansion, if executed well, can create tremendous shareholder value.

Of course, no investment is without risk. Prairie is still a small-cap, relatively speculative venture in a cyclical industry. Challenges like integrating a large acquisition, managing debt from the deal, and executing an ambitious drilling program lie ahead. Commodity prices can swing, and operational hiccups can occur (as with any oil producer). Volatility should be expected. Yet, for bullish investors, the thesis is that Prairie’s upside potential outweighs these risks. The company now has the assets, team, and funding to substantially increase its cash flows in the next 1-2 years. If it delivers on the 2025 plan and beyond, today’s valuation could end up looking like a bargain.

In a way, Prairie Operating Co. represents the quintessential “oil patch underdog” – a smaller player taking bold steps to grow in an industry dominated by giants. And as history has shown, sometimes these underdogs strike it rich. With a transformative acquisition on deck, robust production growth, and supportive industry trends, Prairie is one to watch in the energy space. For investors with a bullish inclination and tolerance for a bit of wildcatting, Prairie Operating offers a compelling mix of high growth, improving fundamentals, and exposure to the ever-valuable commodity that keeps the world running. It’s still early innings, but this is one junior oil company that’s drilling for big gains – and just might hit the mark.

Disclaimer

The information provided in this video about Prairie Operating Co. is for informational and educational purposes only. It does not constitute financial advice, investment advice, or a recommendation to buy or sell any securities. Viewers are encouraged to conduct their own independent research or seek advice from a licensed financial professional before making any investment decisions. If you want to learn more about Prairie Operating Co., visit their investor page for more information.

Cashu Technologies Pty Ltd has been compensated $2,750 by Virtus Media Co. on behalf of Prairie Operating Co. for this promotional content. While we have taken care to present accurate information, we make no guarantees as to the accuracy, completeness, or reliability of the information provided. Any investment decision you make based on this video is at your own risk, and Cashu Technologies Pty Ltd assumes no liability for any losses or damages that may result.