The “Made in America” story most companies only pretend to be

Here's why we're watching this stock.

Not investment advice. Disseminated on behalf of Worksport Ltd.

Most small-cap “American manufacturing” stories are faking it.

The product’s made overseas, the supply chain is fragile, and the only thing that’s truly domestic is the press release.

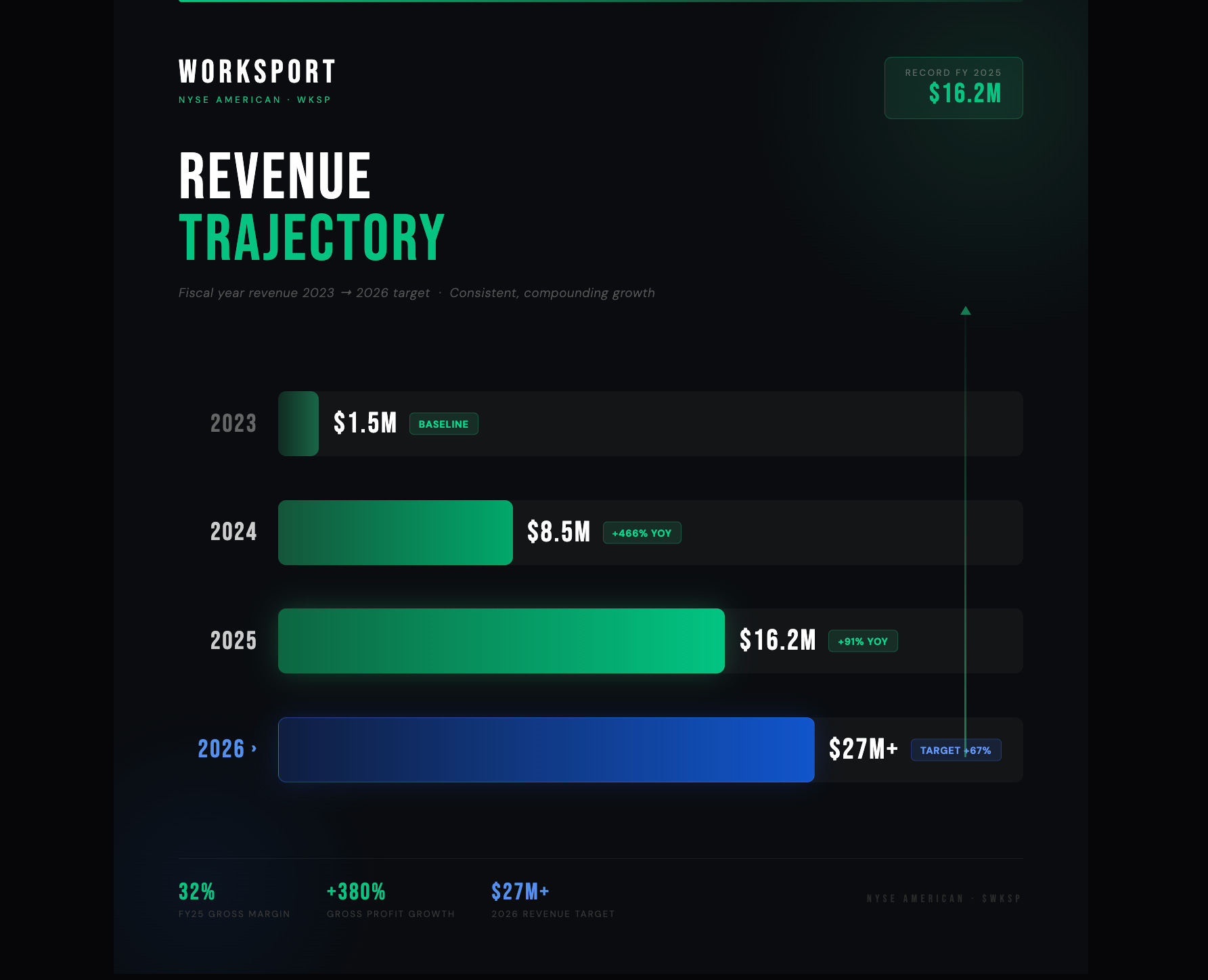

Worksport (NASDAQ: WKSP) is building the kind of story that’s harder to fake: real U.S. production, real operational leverage, and financial signals that suggest it’s moving from “building” to “executing.” In its February 11, 2026 preliminary update, the company reported Q4 2025 gross margin of 32%, up from 11% in Q4 2024, alongside Q4 revenue of $4.84M (+65% YoY) and FY 2025 revenue of $16.2M (+91% YoY).

That matters because, in the real world, “Made in America” isn’t a slogan… it’s a cost structure. It’s quality control. It’s how fast you can iterate. It’s whether you can actually deliver when demand shows up.

And Worksport’s foundation is a very tangible one: a 222,000 sq. ft. manufacturing facility outside Buffalo, New York, paired with ISO 9001:2015 certification—the kind of credential that signals the company is building toward consistent, scalable production standards.

Once you have that base, the story gets more interesting. Because Worksport isn’t just trying to sell truck accessories. It’s trying to turn the pickup truck into a platform—one that can generate, store, and use power in a way that fits how people actually live and work.

From “small accessories company” to a real manufacturing platform

Worksport’s transformation is easiest to understand with one image: a 222,000 sq. ft. manufacturing facility in West Seneca, New York, outside Buffalo. According to the company, this facility has the capacity to support $100M - $300M in annual revenue.

That facility has been central to the company’s pivot toward in-house production and quality control, including achieving ISO 9001:2015 certification, a signal the company believes supports OEM-grade manufacturing credibility and scalability.

This matters because it’s one thing to sell a product. It’s another to build the capability to produce at scale, control your costs, and keep improving the economics of every unit.

And according to Worksport’s latest preliminary Q4 release, that’s where the story starts to show up in the numbers.

The Q4 print that changed the tone

On February 11, 2026, Worksport reported preliminary unaudited results showing:

Q4 2025 net sales of $4.84M, up 65% YoY

Q4 gross margin of 32%, up from 11% a year earlier

FY 2025 revenue of $16.2M, up 91% YoY

For a company like this, the revenue growth gets attention, but the margin expansion is the real tell. It suggests the factory isn’t just “there.” It’s starting to do what factories are supposed to do: absorb fixed costs, reduce per-unit cost, and turn scale into operating leverage.

That’s the kind of foundation retail investors often miss early because it’s not as flashy as a new product launch. But it’s what makes new product launches matter when they arrive.

The product angle: turning a pickup truck into a mobile power system

Now for the part that makes Worksport feel like more than an accessories manufacturer.

The company has been building around pickup trucks, not just as utility vehicles, but as the next surface area for distributed energy. If you’re a contractor, a fleet operator, or even just someone who has lived through a blackout, you understand the problem immediately:

Power isn’t always where you need it.

Worksport’s clean-energy lineup aims to make the truck bed part of the solution. The company has launched:

SOLIS, a truck-mounted folding solar tonneau cover

COR, a portable battery system designed to pair with SOLIS

In December 2025, Worksport announced the launch of COR and SOLIS online sales, framing it as a compact “nano-grid” concept for use cases like worksites and emergency power. A more recent company blog post continues to market the system as modular, solar-powered energy intended for real-world scenarios (jobsites, emergencies, travel), with assembly referenced at its ISO-certified New York facility.

This is the important retail framing: Worksport isn’t trying to win the “coolest camping gadget” category. It’s trying to attach energy functionality to something millions of Americans already own and use every day.

If they execute, that’s a very different market conversation than “we sell truck covers.”

The second swing: HVAC and cold-weather performance

Then there’s Terravis Energy—Worksport’s subsidiary focused on heat pump technology.

If you’ve ever talked to someone in a cold climate about heat pumps, you hear the same objection: performance when it’s brutally cold.

In October 2025, Worksport announced that Terravis Energy was selected for a project under NREL’s Technical Assistance Program (NTAP) in Alaska to analyze its AetherLux™ Pro heat pump with ZeroFrost™ technology, in collaboration with NREL (a U.S. DOE national laboratory).

This isn’t the same thing as a commercialization guarantee, but it is meaningful validation that the company’s cold-weather thesis is being evaluated through a federal lab framework.

For retail investors, that’s the point: the company is taking on real, practical pain points, power access and heating efficiency, where “better” isn’t a luxury feature. It’s a functional upgrade people can feel.

The “why now” tension

Here’s what makes Worksport compelling in early 2026:

The company has moved from “setup” to “proof of execution,” with Q4 margin expansion and record annual revenue.

It has launched clean-energy products that move the thesis from “concept” into “commercial.”

It has a second technology track (Terravis/AetherLux) that has attracted NREL program engagement.

And importantly, Worksport has also communicated improved funding runway through a $10M Regulation A raise announced in October 2025, which the company framed as removing near-term capital uncertainty as it targets cash-flow positivity timelines.

None of this guarantees the outcome. But it does create urgency of a different kind…The “pay attention while the story is turning from build phase to monetize phase” kind.

Because once a company proves it can manufacture, protect margins, and ship the products, the market tends to start treating it differently.

The bottom line

Worksport (WKSP) is trying to become a rare thing in small-cap land: a company that can legitimately say it’s building American manufacturing capacity and layering technology-driven products on top of it.

The early 2026 setup is straightforward:

A real factory platform in New York, now ISO-certified

Financial momentum highlighted by Q4 2025 preliminary results (revenue growth + margin expansion)

Clean-energy products (SOLIS + COR) now commercially launched

A parallel HVAC initiative being analyzed with NREL NTAP involvement

If you want the deeper breakdown, the right way to follow this story is not by asking “will it moon?”

It’s by tracking execution: production scale, margin durability, SOLIS/COR adoption, distribution expansion, and whether the Terravis track keeps turning into credible milestones rather than just R&D.

That’s how real operating stories get built, one quarter at a time.

Disclaimer: This content was produced on behalf of Worksport Ltd. and sponsored by the company. We were compensated by Worksport Ltd. to create this content. This is not financial advice, and viewers are encouraged to consult a financial professional before making investment decisions. Investing in companies involves significant risks, and past performance does not guarantee future results. Please do your own research.