The Team Behind Four Uranium Discoveries Just Started Over at a $6M Market Cap

Why F4 Uranium might be the most asymmetric bet in the Athabasca Basin right now

Not investment advice. Disseminated on behalf of F4 Uranium Corp.

(TSXV: FFU | OTCQB: FFUCF)

Small-cap uranium stocks have a history of creating millionaires.

Not the slow-compounding kind. The kind where a drill hole hits high-grade in the Athabasca Basin and a micro-cap re-rates before most people even knew it existed.

That’s happened before. More than once. And the same team keeps showing up.

Fission Energy(F1) got acquired by Denison Mining. Fission Uranium (F2) got taken over by Paladin Energy in a headline $1.14B transaction. F3 Uranium made two new uranium discoveries in the Athabasca Basin and trades around a ~$100M market cap today.

F4 Uranium (🇨🇦FFU / 🇺🇸FFUCF) is the newest vehicle from that same lineage. It trades at roughly $0.08 a share with a market cap under $10M, making it one of the smallest uranium exploration companies on the TSX Venture Exchange.

Investors might look at that and think: “That’s the whole company?”

Yes. And that’s exactly the point.

The same dynasty. A fraction of the price.

F4 isn’t a new team rolling the dice in an unfamiliar basin. It’s the same group who built F1, F2, and F3, the “Fission Dynasty,” now running the smallest, earliest-stage vehicle in the lineage.

This team is responsible for four major Athabasca Basin discoveries: the J Zone at Waterbury Lake (2010), the Triple R deposit at Patterson Lake South (2012), the JR Zone at Patterson Lake North (2022), and the Tetra Zone at Broach Lake (2024).

When F1 exited at approximately $70M and F2 culminated in a $1.14B transaction, both started as micro-caps that most investors dismissed. The question isn’t whether this team can find uranium. They’ve proven they can, four times. The question is at what price you want exposure.

16 properties. $6.63M market cap. Do the math.

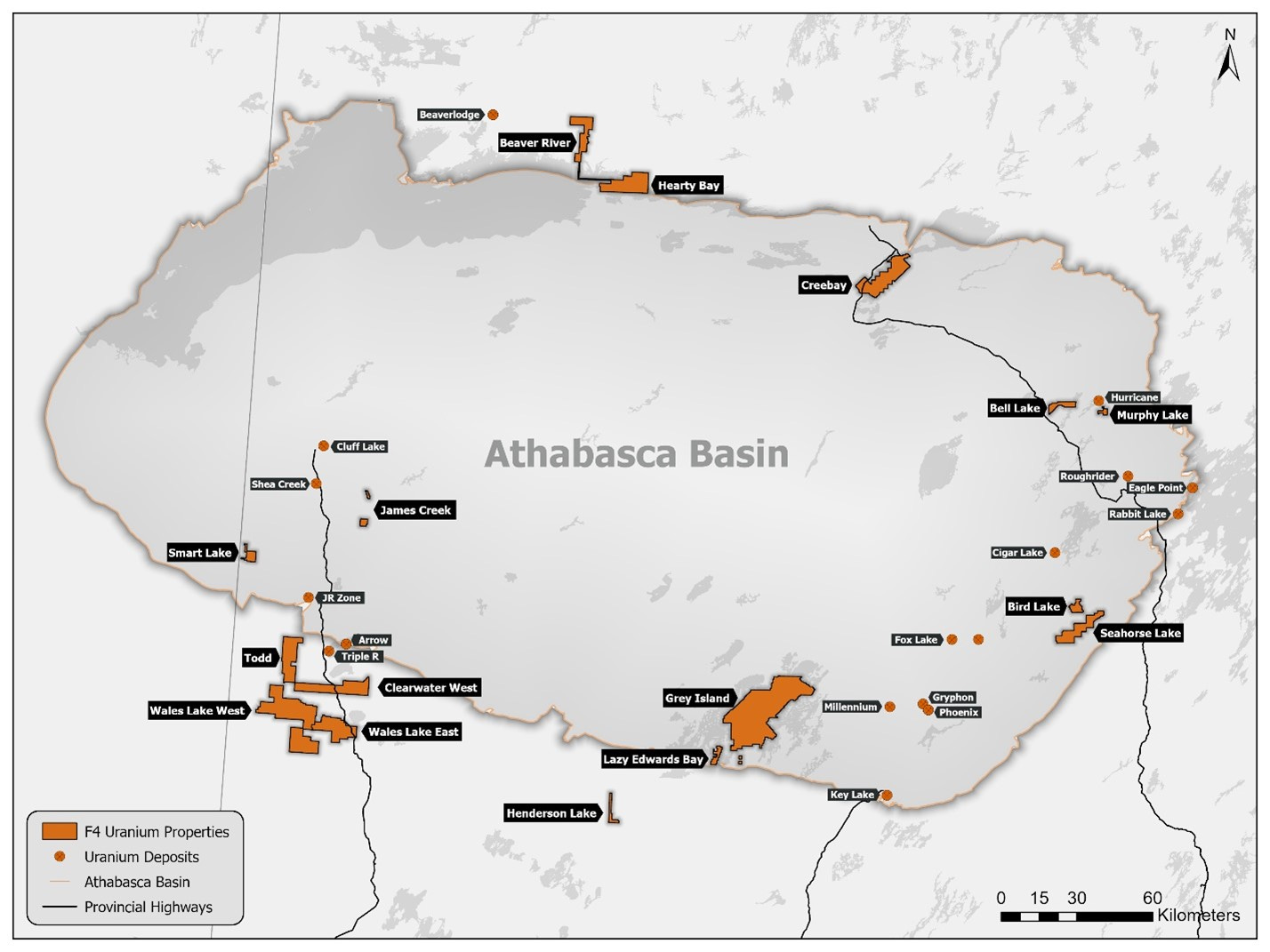

F4 holds approximately 16 uranium exploration projects across the Athabasca Basin, including Murphy Lake, Todd Lake, Wales Lake, Grey Island, Clearwater West, and more.

A $6.63M market cap spread across 16 properties means the market is pricing each one at roughly $400K. A single high-grade intercept at any of them can re-rate the entire company overnight.

That’s not a flaw in the story. That’s the thesis.

Surrounded by giants, with drills turning this summer

Location is everything in the Athabasca, and F4’s flagship properties sit next to some of the biggest names in uranium.

Murphy Lake is 5 km south of ISOEnergy’s Hurricane Deposit, 4 km east of Cameco’s La Rocque Lake Zone (where one hole hit 29.9% U₃O₈ over 7.0m), and 30 km northwest of Orano’s McLean Lake deposits.

Todd Lake and Wales Lake sit within 25 km of Paladin’s Triple R and NexGen Energy’s Arrow deposits. Wales Lake lies southwest of the Dirkson and Saloon Trends, and with F3’s Tetra Zone discovery in 2025 validating the Clearwater Domain, the company believes it carries meaningful analogous upside.

Remember, this is the same team that discovered the Triple R deposit that eventually sold to Paladin. They know this geology better than almost anyone.

Drilling at Murphy Lake is set to begin at the end of May 2026, funded by partner UraniumX Discovery Corp. under an earn-in agreement, followed by work at Todd Lake.

Funded exploration without diluting shareholders

F4 has signed a definitive option agreement with UraniumX Discovery Corp. (formerly Stearman Resources Inc.) to earn up to a 70% interest in Murphy Lake by spending $18M. That means F4 gets its flagship property drilled largely at someone else’s expense.

Flow-through financing further reduces costs, allowing F4 to chase multiple targets without diluting shareholders to fund the work.

In junior mining, “who’s paying for the drill program” is half the story. At Murphy Lake, the answer is not F4 shareholders.

New geophysics on untested ground

In February 2026, F4 completed an airborne geophysical survey over the Grey Island Project, identifying multiple prospective target corridors. Grey Island sits 70 km west of the Key Lake Mine and 60 km east of Cameco’s Centennial deposit, with only one historical drill hole on record.

Modern tech, limited prior drilling, proximity to major operations. That’s the combination Athabasca discoveries are built on.

The spin-out playbook that keeps working

In August 2024, F3 spun out F4, handing it 17 prospective uranium projects. F3 kept its high-conviction PLN project, the JR Zone and Tetra Zone, and packaged everything else into the new vehicle. That “everything else” now trades for $6.63M.

The playbook from F1 to F2 to F3 has been consistent: spin out early, explore aggressively, make a discovery, attract a major. F4 is the latest iteration, at the earliest possible stage.

F3 already has a resource, with a market cap of ~$100MM. F4 has 16 properties, none of that priced in, at $6.63M. The upside on a discovery is orders of magnitude larger relative to the entry point.

At $0.08 per share, you’re not paying for a discovery. You’re paying for the option on one, made by the same people who’ve done it four times before.

The bottom line

F4 Uranium (🇨🇦FFU / 🇺🇸FFUCF) is the earliest-stage vehicle from the most successful uranium discovery team in the Athabasca Basin.

A proven team with four discoveries. 16 properties in a single micro-cap. Drill catalysts starting this summer. Funded exploration that doesn’t dilute shareholders. And a market cap under $10M that prices each property at roughly $400K.

If the pattern from F1 through F3 repeats, the re-rating happens before the market catches on. That window, when the team is assembled, the properties are loaded, the drills are funded, but nobody’s paying attention yet, is exactly where F4 sits today.

The ticker is FFU on the TSX Venture, or FFUCF on the US OTC.

Disclaimer: Disseminated on behalf of F4 Uranium Corp. This newsletter is for informational purposes only and is not investment advice. It is part of a paid marketing campaign. Cashu Group was compensated by F4 Uranium Corp. through a third party marketing firm for the creation and distribution of this content. Investing in early-stage exploration companies is speculative and involves significant risk, including the risk of loss of capital. All project details, share counts, and financial figures referenced come from the company’s public disclosures. Always do your own due diligence and consult a licensed financial professional before making investment decisions.