Victory Metals (ASX:VTM): Building the West’s Next Strategic Rare Earth Supply Source

Building the West’s Next Strategic Rare Earth Supply Source

Rare Earths Are No Longer Just Commodities

For years, rare earths sat in the background of the resources sector, niche, misunderstood, and largely ignored. That has changed.

Today, they sit at the centre of three of the most important global trends: defence capability, energy transition, and supply chain security.

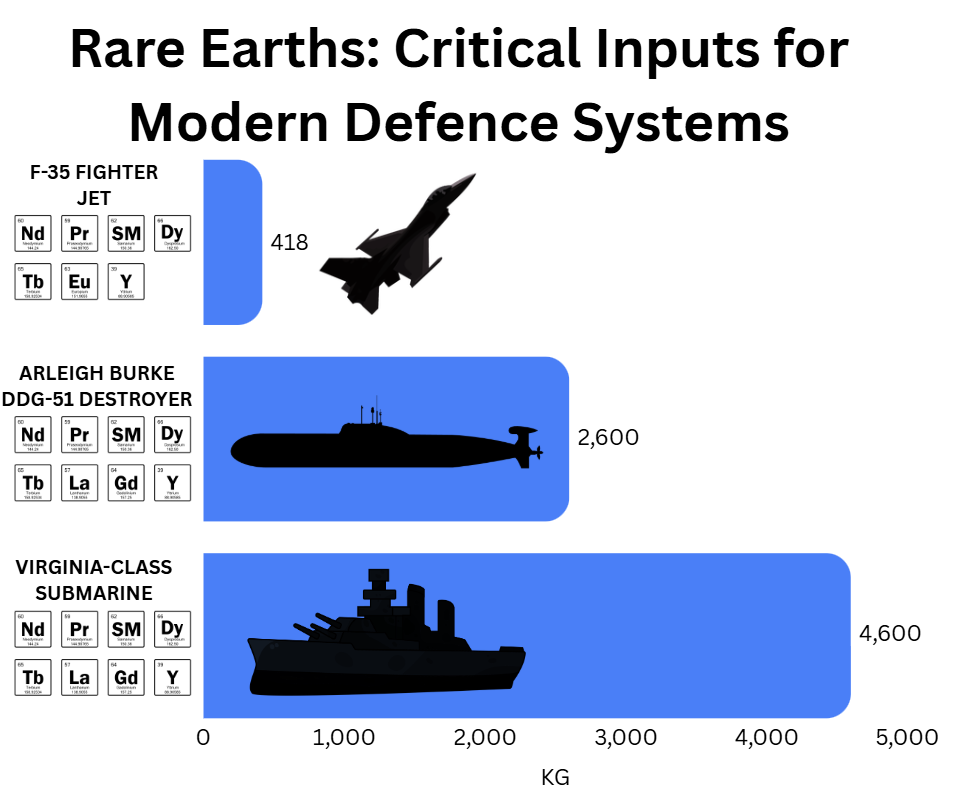

Heavy rare earth elements like dysprosium and terbium are critical inputs in high-performance magnets. These magnets power everything from F-35 fighter jets and missile systems to electric vehicles and offshore wind turbines. There are few substitutes, and supply remains highly concentrated.

That concentration has become a problem. Recent policy shifts have made it clear that rare earths are no longer just a commercial issue, they are a strategic one. Governments are now actively looking to secure alternative sources of supply, particularly in Western-aligned jurisdictions.

This is the backdrop in which Victory Metals is operating.

A Rare Western Heavy Rare Earth Asset

Victory Metals’ North Stanmore project, located in Western Australia, stands out for one simple reason: it is exactly the type of project the market is now looking for.

It is a large-scale, clay-hosted deposit with a high proportion of heavy rare earths, the most supply-constrained and strategically valuable part of the market. The resource currently sits at 320.6 Mt at 510 ppm TREO, with a strong heavy rare earth component and mineralisation still open.

Importantly, the geology works in its favour. This is soft, free-digging clay, meaning no blasting, no complex mining, and a relatively straightforward processing pathway. Infrastructure is already in place, with access to roads, rail, and ports.

The initial scoping study outlined a A$1.2 billion NPV and 52% IRR, positioning the project as economically robust even before recent technical improvements.

And those improvements are where the story gets more interesting.

A Project That Is De-Risking Quickly

Over the past year, Victory has delivered a series of results that materially change how the project should be viewed.

The most significant is the 48x flotation upgrade, which dramatically increased concentrate grade while rejecting the vast majority of waste upfront. Alongside this, test work has shown that roughly 80% of rare earths can be leached within ~30 minutes, far faster than typical assumptions.

Taken together, these results suggest a project that could be simpler, smaller, and cheaper to build than originally expected.

At the same time, the company has begun to attract strategic validation. A US EXIM Letter of Interest for up to US$190M and a non-binding LOI with Sumitomo indicate that the project is already being recognised as part of a broader push to secure non-Chinese supply.

This combination, improving technical confidence and growing strategic interest, is what typically drives re-ratings in development-stage resource stocks.

The Investment Case

At its core, the investment case for Victory Metals rests on a simple disconnect.

The market is still valuing the company like a typical early-stage developer, while the underlying project is increasingly being treated as a strategic asset.

North Stanmore offers:

exposure to heavy rare earths, the most supply-constrained segment of the market

a low-intensity development pathway through clay-hosted geology

improving economics driven by recent metallurgical breakthroughs

early signals of government and strategic partner support

a clear pipeline of near-term catalysts, led by the Q2 2026 PFS

At around A$1.40 per share, the stock trades at a deep discount to its scoping study value. In our view, that discount does not fully reflect either the technical progress made or the strategic relevance of the asset.

Bottom Line

Victory Metals is no longer just a speculative exploration story.

It is becoming a strategically relevant rare earth project at a time when the world is actively searching for exactly this type of supply.

With improving project fundamentals, growing external validation, and a catalyst-heavy next 12 months, we see a clear pathway for a meaningful re-rating.

Disclaimer

We provide only general financial product advice. You should note that general advice does not relate specifically to you and is prepared without taking into account any of your objectives, financial situation or needs. As a result, before acting on the general advice, you should consider the appropriateness of the advice, having regard to your objectives, financial situation and needs. You should consider seeking the advice of relevant legal, taxation, superannuation, financial and/or other relevant advisors before the information is acted on. The general advice provided relates to securities which are listed on an exchange (usually the Australian Stock Exchange). You should consider any information published by the listed company (including, without limitation, any prospectus, ASX announcements, or other investor updates published by the relevant company) before acquiring or investing in any shares. Whilst Cashu Research has taken reasonable care, there is no guarantee by either Cashu Research, or its AFSL provider, ASG, that the information in this Research Report is accurate or up to date. Cashu Research or Cashu Group may receive fees for research or corporate communication services from companies mentioned in this report. Cashu Research, its directors, employees or associates may hold or trade securities in these companies and may change such holdings without notice. The general advice in this Research Report is provided by Cashu Research. Cashu Research is part of Cashu Technology Pty Ltd, which is an authorised representative (AR # 001318029) of Adviser Solutions Group Pty Ltd (ABN 88 601 875 521) (AFSL 485946) (ASG). Report prepared by Cashu Research, a division of Cashu Group. This report has been authored and issued by the analyst(s) named herein.